The Market

Wind Propulsion Market Overview

There has been a steady growth in market interest for wind propulsion solutions. This market interest has been driven by a number of key factors, including the IMO initial strategy on reducing GHG emissions in shipping by at least 50% by 2050, but also by market leaders taking zero emissions stances, including Maersk’s pledge to cut carbon emissions to zero by 2050.

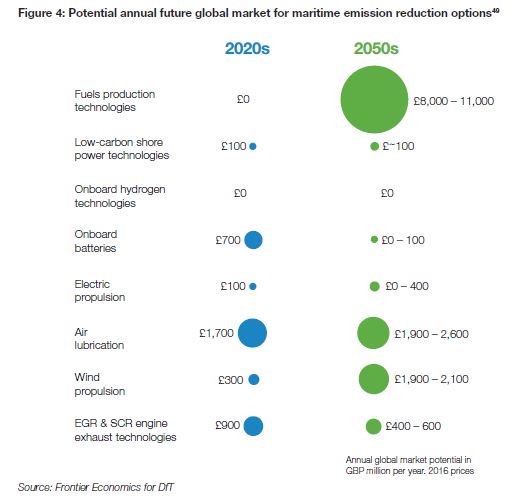

The UK Government’s Clean Maritime Plan (released in July 2019), has assessed the global market for wind propulsion systems, and this is estimated to grow from a conservative £300 million per year in the 2020s to around £2 billion per year by the 2050s worldwide.

The Frontier Economics Report (July 2019) REDUCING THE MARITIME SECTOR’S CONTRIBUTION TO CLIMATE CHANGE AND AIR POLLUTION: Economic Opportunities from Low and Zero Emission Shipping. A Report for the UK Department for Transport adds further detail (page 43-44), forecasting that the market size by 2050 (assuming 50-100% abatement of GHG) for wind propulsion would be 37,000 – 40,000 vessels with wind propulsion systems installed or roughly 40-45% of the global fleet.

The market potential for wind propulsion was also assessed in an EU commissioned report produced by CE Delft and associates. ‘Study on the analysis of market potentials and market barriers for wind propulsion technologies for ships’. [Note: This report was compiled in 2016-17 prior to much of the SOx regulation uptake and over a year before the IMO GHG initial strategy adoption]

The headline findings were: ‘Should some wind propulsion technologies for ships reach marketability in 2020, the maximum market potential for bulk carriers, tankers and container vessels is estimated to add up to around 3,700-10,700 installed systems until 2030, including both retrofits and installations on newbuilds, depending on the bunker fuel price, the speed of the vessels, and the discount rate applied. The use of these wind propulsion systems would then lead to CO2 savings of around 3.5-7.5 Mt CO2 in 2030 and the wind propulsion sector would then be good for around 6,500-8,000 direct and around 8,500-10,000 indirect jobs.’

This would be a significant low carbon technology penetration into the fleet, and these calculations were made prior to significant regulatory decisions in 2018/19. As it currently stands, there are a number of ready for market wind-assist technology providers in the retrofit market, with an increasing number of retrofit installations of proven rotor technology and test rigs and a growing number of other retrofit technologies and newbuild designs are in late stage R&D or moving towards sea trials.

As we approach 2024, there are significant market drivers that are will influence the price of fuel and the availability of compliant fuel worldwide. Oil prices have fluctuated quite a lot over the last two year, the world sulphur directive came into force in 2020 and led to a significant increase in costs either ULSFO, with standard HFO users needing scrubbers or have switched to either lighter distillates, LNG or other more costly fuels. The IMO also sent a clear industry decarbonisation message with it’s agreement on preliminary GHG targets in April 2018, of at least 50% cuts (from a 2008 baseline) by 2050. This target may well be tightened further in 2023 and a raft of short term measures came into force in 2023, especially EEXI and CII. The discussion around long-term measures including some form of carbon levy or other market based mechanisms should be concluded at IMO in 2023.

The possibility of mandated speed limits, an HFO ban in the Arctic and the further development of credible and viable hybrid wind and secondary renewable fuel solutions are also having an impact on the industry in it’s search for the next generation technology toolbox. With the development of innovative finance models, where CAPEX is reduced significantly or eliminated completely, there will be increased interest to utilise a technology segment that can deliver 5-20%+ reductions in fuel (and GHG emissions) for retrofit and from 30% and above for optimised new build vessels.

While shipping is currently not included in carbon pricing mechanisms this will change with the inclusion of shipping into the EU Emission Trading System (ETS) from 01 January 2024. This will include 100% of all inter-EU voyages for vessels over 5,000GT and 50% of emissions from voyages including one EU port. These charges will be introduced gradually with 40% payable in Year 1, rising to 70% in Year 2 and 100% by Year 3. There will be further discussions at IMO on an international systems that may follow some of the EU elements. There has been a significant upward pressure on the price of carbon on the EU ETS over the last few years and the indications are that this upward pressure will continue, with the price fluctuating between EUR80-100/tn of CO2 in 2022/23 [1 tn of fuel = c.3.1 tn of CO2]

Combining wind propulsion technologies with voyage optimisation along with secondary renewables such as 2nd generation biofuel (derived from waste), batteries, hydrogen, methanol or ammonia etc., and a suite of ship efficiency technologies can deliver significantly reduced carbon shipping, putting the industry on a path towards full decarbonisation, even under tight GHG emission reductions scenarios.

General Market Overview

World Seaborne Trade

• According to the International Chamber of Shipping (ICS), around 90% of global trade is carried by sea. Shipping & World Trade (ICS).

• UNCTAD noted that world seaborne trade bounced back in 2021, Shipments grew by an estimated 3.2% to reach 11 billion tons. This represents an improvement of 7% compared with the 3.8% decline in 2020. UNCTAD Review of Maritime Transport (2022)

• Dry cargo (dry commodities carried in bulk, general cargo, breakbulk and containerized trade) accounts for around 70%, while the tanker trade (crude oil, petroleum product and gas) was c.30%.

World Commercial Fleet Size

• World fleet totalled 2.2 billion dwt. in January 2022.*

• Bulk carriers (42.9%) of the total tonnage. Oil tankers (28.5%) Container ships (12.8%).

• World fleet numbers (depends on source & calculation method) – cargo-carrying vessels are between 55,000-60,000, all vessels excluding those listed below is between 80,000-90,000 and the IMO gives numbers over 100,000 (including large fishing vessels)

(*above 100GT, excluding inland waterway vessels, fishing vessels, military vessels, yachts and offshore fixed and mobile platforms and barges (with the exception of floating production storage and offloading units and drill ships)

Merchant fleet by flag of registration

Merchant fleet by country/economy of ownership

World Fishing Fleet Size

• Total number of fishing vessels is estimated by FAO at 4.72 million in 2012. Asia (68%), Africa (16%).

• 3.2 million vessels were considered to operate in marine waters.

• 57% of fishing vessels were engine-powered.

• 70% of marine-operating vessels were engine-powered (regional variations)

• 79% of the motorized fishing vessels were less than 12m length overall (LOA).

• Industrialized fishing vessels of 24m and larger operating in marine waters was about 64,000.

FAO: the State of the World Fisheries & Aquaculture